- What We Do

- Who We Help

- Insights and Resources

- About Us

- Careers

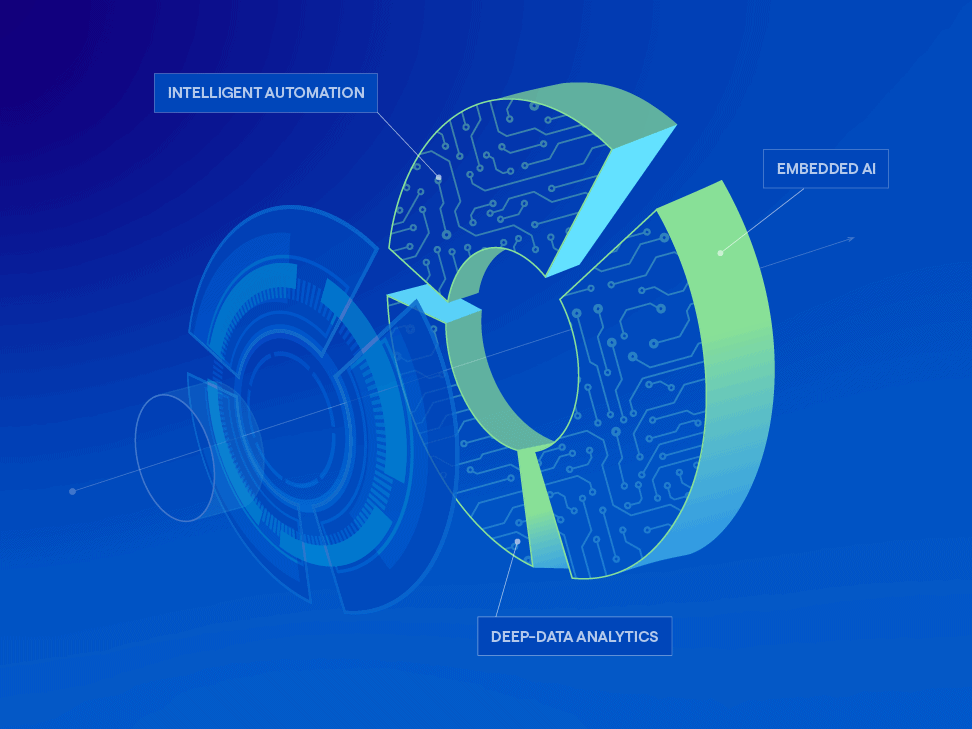

Reimagine the revenue cycle with a future-ready platform

The R1 Platform brings the power of AI, Intelligent Automation and Deep Data Analytics to healthcare through proprietary RCM optimization engines that turn complex data into financial and operating performance improvements – enabling leading healthcare organizations to deliver outstanding patient care today and in the future – with confidence

Where deep RCM experience meets intelligent technologies

The R1 Platform was purpose-built by seasoned revenue cycle operators to bring the industry’s most intelligent technologies, proprietary RCM optimization engines and advanced analytics to transform the revenue cycle.

With data at the core fueling R1’s AI and automation capabilities, the R1 Platform employs optimization engines to uphold accuracy, efficiency, and compliance across the revenue cycle, enabling our clients to stay at the forefront of a rapidly evolving financial landscape.

R1 Embedded AI uses real-time data and several forms of AI including machine learning, natural-language processing and generative AI, to deliver more automation, increased productivity and greater patient satisfaction.

R1 Intelligent Automation unlocks the equivalent of 5,000 FTEs in operational capacity by automating routine and repetitive activities, optimizing workflows and improving team productivity.

The R1 Platform uses data and analytics to improve reimbursement and drive efficiency, leveraging access to data from over 90 of the top 100 health systems and more than 550M patient records accessed nationally per year.

Encompassing more than 20,000 algorithms derived from our work with 95% of US payers and every major EMR, the R1 Rules Engine enforces and automates complex revenue cycle processes to optimize user workflow and maximize revenue opportunities with accuracy and compliance.

Acting as the revenue cycle’s “central nervous system,” our Workflow Orchestration Engine coordinates and optimizes the myriad of steps required to drive financial outcomes by seamlessly blending automated and human-centric workflows.

R1 Contract Modeling and Pricing validates reimbursement accuracy, simplifies contract management, helps recover underpayments and streamlines workflow to ensure that health plans are complying with their contract terms and are being reimbursed appropriately.

A strategic alliance to propel generative AI for the revenue cycle

LEARN MORER1 and Microsoft joined forces to accelerate the development and integration of generative AI into R1’s industry-leading RCM platform. By combining R1’s deep revenue cycle data and expertise with Microsoft’s AzureAI, R1 clients will realize immediate benefits that benefit providers and the patients they serve.

The platform engineered to optimize your revenue cycle at scale

Efficiency at every step

R1’s Platform is at the forefront of innovation, purposefully integrating data and creating a virtuous feedback loop that optimizes every facet of the revenue cycle.

With each data interaction, our intelligent and proprietary technology, coupled with deep connections, workflow and analytics capabilities, unlocks revenue opportunities efficiently and drives results at scale.

Bridging data in a seamless way

The R1 Platform is a data powerhouse that integrates and unifies millions of clinical, financial and patient datapoints to enable accurate, reliable and secure information exchange, across all data sources.

R1’s Unified Data Exchange is designed to integrate with every major EMR, payer, clearinghouse, bank and other data sources. This fluid transfer of data has hundreds of pre-built connections to integrate with multiple data sources, helping to simplify implementation, uphold data integrity and facilitate a seamless connection to the source of truth.

Data that speaks for itself

Intelligent automation

manual tasks automated

200M+

Proprietary rules

rules and algorithms

20K+

Data scale

NPR claims processing visibility

$900B+

Patient records

records accessed annually

550M+

Unlock insights. Maximize results. Stay ahead.

Processing over 550 million patient records annually, R1 is a data powerhouse leveraging real-time data to optimize every aspect of the revenue cycle. With advanced analytics and predictive capabilities, we deliver instant insights, performance transparency and can forecast trends, empowering providers to maintain a competitive edge.

With R1’s data-driven intelligence, our clients have a strategic advantage to maximize performance and stay one step ahead of the curve.

R1’s Platform recovers more revenue than any other RCM partner

At R1, we deliver more savings and recover more revenue than any other RCM company. Our platform runs on deep data, integrated analytics and sophisticated automation, which accompanies decades of expertise to proactively identify problems across your revenue cycle, with comprehensive solutions that drive scalable, sustainable results for you and your patients.

Pure performance, end-to-end

Our platform gives you the power to transform every part of your revenue cycle with user-friendly tools, seamless interoperability and an experienced team.

Expansive data, unmatched results

Our platform, purpose-built by RCM experts, leverages our expansive data access and advanced analytics to drive revenue recovery and accelerate cash flow.

Intelligent technology, durable results

We integrate the latest technologies into a single, powerful platform that drives efficiency from patient access to claims and reimbursement.

Deep expertise, comprehensive solutions

Our highly skilled team of deep domain experts leverage technology and deliver comprehensive solutions that meet your needs.

The latest from R1

EXPLORE ALL INSIGHTS - Who We Help